Option expiration week is one of those “love it or hate it” times in the market. I love it as that’s when I reap the majority of my rewards for selling front-month premium in the $SPX. One of the most difficult obstacles I face is not letting my bias cloud my objectivity. To help lessen the chances of making biased trades I track (or let others do it for me and I subscribe to their newsletters) quite a few statistics. As an example, one would think that after a big down week prior to opex that market makers and others would tend to make more money if the market moved higher. Not the case at all.

There is no room for biases in trading, especially in a market environment like we are currently witnessing. It’s OK to catch yourself trading on opinion, closing the trade for a small loss and moving on. What’s not OK is to hang on to losses because the market “should” do this or that.

Another way I use those statistics I mentioned earlier is to gauge my risk. If there are an increasing number of tendencies that don’t play out then I know the market is highly abnormal and thus I reduce my risk. Perhaps a technical level that has been support/resistance in the past will not be this time and thus I move further out. Simple? Yes, but what’s wrong with that?

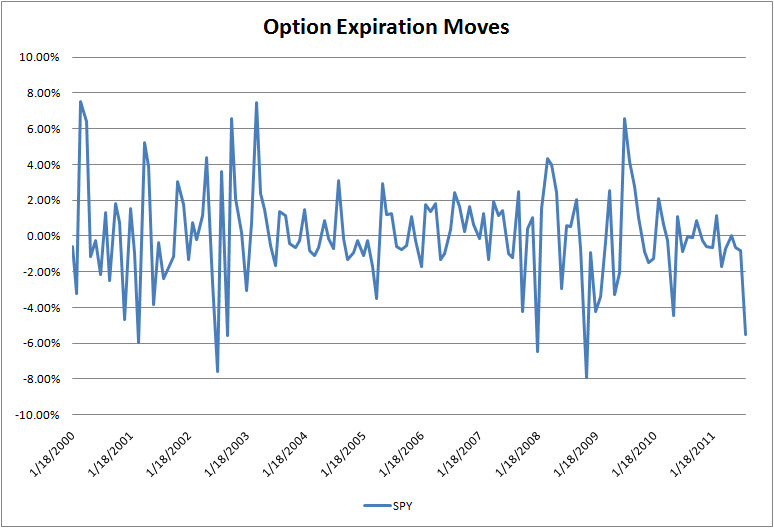

Here are some interesting facts about option expiration week since 2000: [list type=square_list]

- The average move over the period is .04%

- There has never been a move larger than +/- 8% (prior week’s close to opex week open)

- The largest loss was -7.94% in 11/08 (was preceded by a -9.02% loss the prior week)

- The largest gain was +7.44% in 3/03 (was preceded by a +1.85% gain the prior week)

- The average loss over the period for the week is -1.7%

- The average gain over the period for the week is +2.8%

- The most negative closes in a row was 8 from 9/04 to 4/05

- The most positive closes in a row was 6 from 7/06 to 12/06

[/list]

{kind=link}

We just need average # of rumors for opex week and we’re all set 🙂